The banking industry’s reputation suffered considerably in the aftermath of the 2008 financial crisis, with the most vociferous backlash coming from the consumer. The need to rebalance the books and respond to costly regulation had led some banks to stem the flow of credit to small and medium-sized entities, avoid investing in the digital customer experience and ultimately resist downward pressure on profitability. Away from the regulatory spotlight, a revolution was under way: Financial technology (‘FinTech’) firms, with a fresh outlook and a customer-centric approach, breathing new life into the financial services industry. A firm grip on the customer experience differentiated FinTechs from incumbents and has been vital to their proliferation. Large financial institutions must now seriously consider whether these disruptive FinTechs are valuable partners or represent “the four horsemen of the e-pocalypse”[1] and the end to their reign as the gatekeeping institutions that dominate the global economy.

A Fresh Approach and an Investment Surge

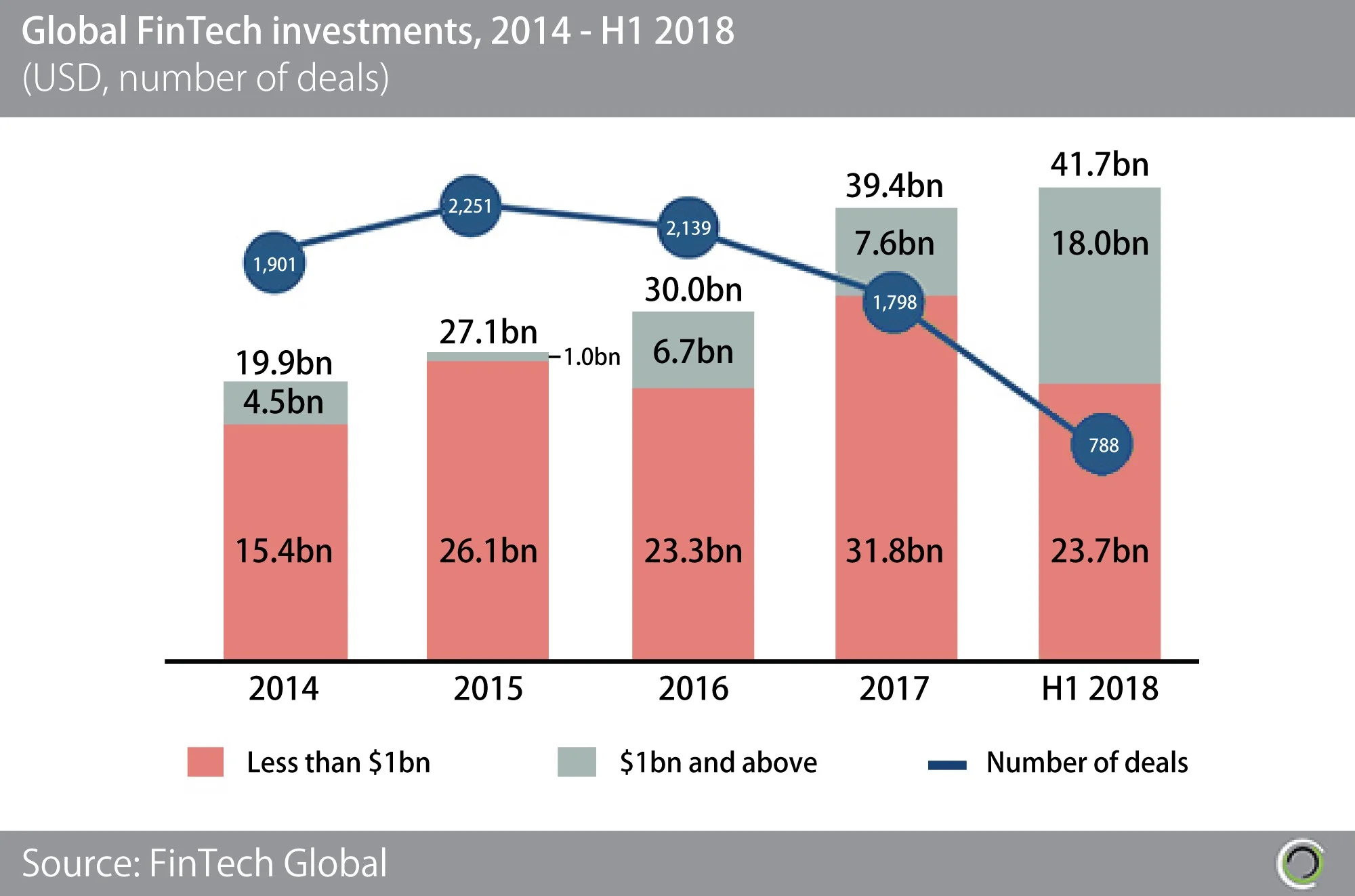

FinTech is a relatively new and burgeoning sector “but in capital markets at least, technology and technological innovation has been a critical part of the financial system for centuries”.[2] Traders’ unquenchable thirst for a competitive edge has been alive and well since the 18th century, with options to facilitate high-speed trade networks being explored and developed at an impressive rate: the telegraph displacing high-speed horses was arguably the most groundbreaking invention of its time.[3] FinTechs have in fact been around for almost two decades, with PayPal often considered the pioneer after its establishment in 1998. However, recent years have seen exponential growth in FinTech start-ups and, according to FinTech Global, “more than $158bn has been invested in FinTech companies globally since 2014, with funding nearing $40bn in 2017”.[4] H1 2018 is already a record year with $41.7bn ploughed into the sector worldwide, surpassing last year’s record total in half the time! (Fig. 1).

Fig. 1

FinTechs have sunk their technologically innovative claws into traditional banking domains such as payments, lending, trading, investing, money transfers and financial planning. The rise of the smartphone and the digitization of the financial services industry has enabled FinTechs to attack different links in banking’s value chain, revolutionizing the way banks interact with their customers. It is FinTechs’ ability to bridge the gap between the services a traditional bank provides and what today’s customer wants that makes them so valuable to the financial services sector.

Friends or Foes?

While it is tempting to perceive FinTechs and incumbents as arch rivals who have locked horns in a battle for supremacy, the opposite seems to be true. When considering their response to this aggressive FinTech surge, the banks had a few options: emulation, collaboration, acquisition or a mixture of all three. Indeed, banks have realized that partnering with and leveraging the customer centric expertise of FinTechs is the most sure-fire way to gain a competitive edge. This is a mutually beneficial relationship, however, with FinTechs also standing a far better chance of survival and growth if they leverage the infrastructure, wealth of data and access to capital that incumbents possess rather than embark on the arduous task of becoming a de novo bank, with regulatory barriers to entry being the most obvious roadblock. Technologies that the capital markets community are leveraging to drive efficiencies, increase revenue and enhance the customer experience include: Cloud Computing, Big Data, Biometrics, Artificial Intelligence (AI), Machine Learning, Open Application Programming Interfaces (APIs), Robotic Process Automation (RPA) and Blockchain / Distributed Ledger Technology (DLT). All stand to drastically change the banking industry as we know it.

Tackling Compliance with Technology

Francisco Gonzalez, Executive Chairman at Spanish banking group BBVA, when arguing that the financial industry was always primed for rapid and early digitization, outlines that its fundamental “raw materials” boil down to two elements: data (or information) and money.[5] Banks are working closely with Regulation Technology (RegTech) innovators, often considered a subclass of FinTech, to harness huge amounts of structured and non-structured data to stay compliant in a regulatory environment that continues to evolve. The AI and machine learning prowess of RegTechs provide incumbents with the ability to analyze large data sets, identify trends, extract necessary data and ultimately prepare robust regulatory reports, which is a welcomed relief for banks feeling burdened by regulatory demands.

Dejan Kusalovic, Global Head of FinTech Enabling at Intel, envisions a “nirvana” state in which RegTechs interoperate with incumbents to facilitate real-time regulatory reporting, smarter risk identification and faster decision making.[6] Cloud technology, cognitive automation and the advent of open APIs (connecting financial institutions, FinTechs and regulators) enable this collaboration to flourish but this is only the tip of the iceberg: investment in new technologies is aiding business agility throughout the financial services industry.

Agility, Automation and Accuracy

Cutting complexity, reducing costs and resolving operational inefficiencies are three items high on the agenda for capital market firms looking to ease pressure on tight margins. Operating across multiple business silos and moving data across a myriad of disparate legacy systems are typical causes of complexity and inefficiency within a bank’s operations. The capital markets community is harnessing the power of intelligent automation and cognitive Robotic Process Automation (RPA) to navigate these hurdles, with middle and back office operations as the key candidates for upheaval.

Throughout the trade lifecycle, functions such as risk monitoring, reconciliation, settlement and reporting require a vast amount of human effort; RPA can ensure these rule-based and somewhat repetitive tasks are completed more quickly and with greater accuracy whilst sustaining an automated audit trail to be used for regulatory purposes. Beyond middle and back office operations, RPA’s autonomous decision-making capability extends to client onboarding in the front office, thus removing the reliance on manual processes around Know Your Customer (KYC) and Anti Money Laundering (AML): two vital due diligence processes. Digitizing the end-to-end trade lifecycle and freeing up the workforce to focus on less repetitive and more interesting strategic endeavors is a huge benefit of RPA adoption. However, some would argue that the ability of RPA to improve upon and leverage a bank’s existing systems, instead of necessitating their expensive replacement, is this new technology’s real silver bullet.

Blockchain / Distributed Ledger Technology (DLT)

Generating excitement and skepticism in equal measure, blockchain technology is transforming financial markets and turning heads in the capital markets community. While best known as the technology behind Bitcoin, blockchain (more broadly, DLT) is essentially an immutable record-keeping database of transactions that is shared across and maintained by members of a decentralized network—hence also being known as a distributed ledger. Each transaction is permanent, with its integrity and security protected by cryptographic encryptions and consensus algorithms. Simply put, the blockchain intends to remove the requirement for third party intermediaries to ensure trust between trading parties. Distributed ledger technology’s promise to bring operational efficiencies and cost reductions to clearing and settlement cycles, payments and the execution of financial contracts (using smart contracts) have left banks scrambling to initiate proofs of concept (POCs) and ultimately adopt this exciting new technology.

Looking at global payments and their susceptibility to disruption, imagine a world in which global inter-bank payments could happen almost instantly, with significantly reduced fees and extremely high security. A distributed ledger attempts to make this world a reality. Operating on a peer-to-peer network, DLT boasts the ability to record a transaction, hold the necessary counterparty data and automatically enact a cross-border payment based on business logic embedded in a smart contract. Not only does such disintermediation introduce greater speed, transparency and security, it also removes the fees associated with the intermediate banks and clearing houses. It is yet to be seen just how disruptive this groundbreaking technology could prove to be, but one thing is for sure: the core infrastructure of capital markets cannot ignore the potential of distributed ledger technology to transform the financial services ecosystem.

Security Concerns

While FinTech has experienced rapid growth, providing the financial services industry with countless new ways to interact with their customer and expand revenue streams, there is a security risk associated with moving more services online. Ironically, innovations such as blockchain and biometrics are designed to enhance security and weed out fraud with their state-of-the-art identity management capabilities. However, these nascent technologies still have a way to go before they are mature enough to be considered impenetrable, and thus potentially open more doors to today’s sophisticated fraudsters.

In terms of data, while increased volumes being shared amongst financial incumbents and third parties is an inevitability as the industry becomes increasingly digital, this in turn raises new concerns over data security and privacy. Without demonstrating robust cybersecurity, fraud and data controls, consumer confidence may begin to fade, easing the current fast-paced adoption of FinTech.

Why Monticello

Monticello Consulting Group has managed some of the most transformational technology programs on Wall Street with services that include data management, testing governance, and program office implementation. Our in-depth knowledge uniquely positions us to guide clients in the deployment of the latest financial technologies – accelerating innovation and reducing risk.

Get In Touch

LEARN MORE ABOUT MONTICELLO AND PURSUE OPPORTUNITIES WITH OUR TEAM

[1]https://www.amundi.lu/professional/ezjscore/call/ezjscamundibuzz::sfForwardFront::paramsList=service=ProxyGedApi&routeId=_dl_NTlkMmRmYThkNTY5Mjk1YzZhNDNmZWFmOGIzMDRiMzQ

[2] Paul Walker, Senior Advisor to Motive Partners and Former Co-Head of Technology at Goldman Sachs

[3] https://www.moaf.org/publications-collections/financial-history-magazine/111/_res/id=Attachments/index=0/Plundered_by_Harpies.pdf

[4] http://fintech.global/2018-is-already-a-record-year-for-global-fintech-investment/

[5] https://www.bbvaopenmind.com/wp-content/uploads/2015/04/OpenMind-Transforming-an-Analog-Company-into-a-Digital-Company-The-Case-of-BBVA.pdf

[6] https://reg.tech/ecomaXL/get_blob.php?name=intel_regtech_finextra.pdf